Do you ever wonder what your dream home would look like? Would it be a high-rise apartment overlooking the city or a nice landed property with lots of space for your pets to run around?

Dreaming is often the easy part. However, do you know what it takes to own your desired home? Let’s cover some of the most important rules that every future owner should know, before signing a mortgage.

Rule 1

Know How Much You Can Borrow and What You Can Really Afford to Spend

First and foremost, before setting off on a hunt for your future house, you must find out how much budget you have available. There’s no point searching for properties you, in the end, can’t afford.

Start with getting a sense of whether the bank will give you a loan in the first place. They are in a position to decline your request for different reasons, don’t forget that!

Secondly, fully understand how much money they are willing to offer you. Combining this with your own savings, should give a clear idea of the budget you will have available. At the same time, understand the monthly instalments this loan will come with to get a full picture of what you’re buying into. Work out a consolidated budget and take into account of all your other monthly costs related to the property. If you, at any point, feel that the mortgage you are buying into will be too heavy to oblige to, then re-consider and change your target budget. You will not enjoy living in your dreamhouse if you start realising that you can’t afford it.

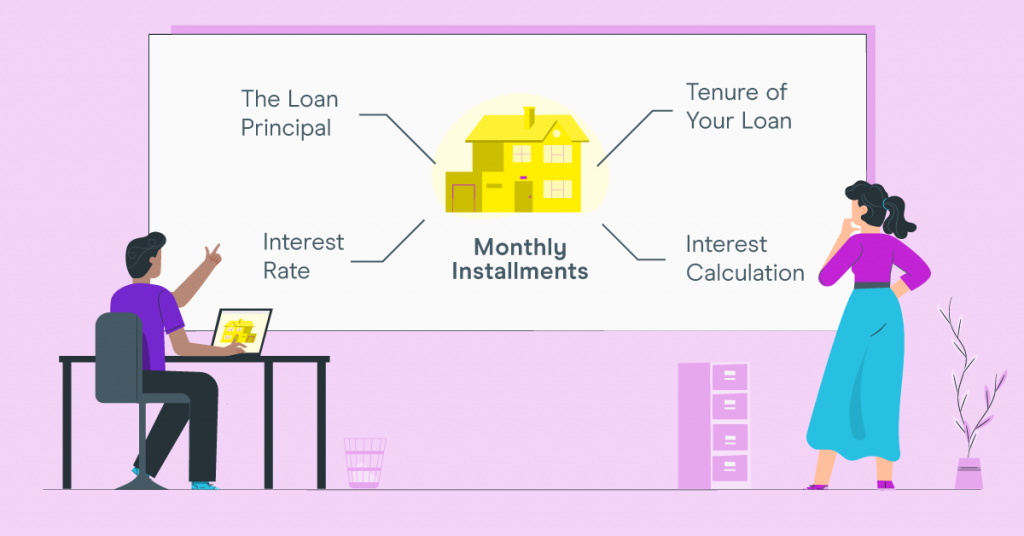

Rule 2

Be Aware of the Monthly Instalments

Speaking of monthly instalments, there are four things to look out for when calculating your monthly mortgage payments: the loan principal, interest rate, tenure of your loan and interest calculation. The loan principal is essentially the amount that you are borrowing and the more you borrow, the more interest you will need to pay. The interest rate of your home loan, on the other hand, is usually based on your bank’s cost of funds, which in turn is regulated by the National Bank of Cambodia. Your monthly repayments are also affected by the tenure of your loan. The longer you take to pay off your loan, the more interest you will have to pay. Lastly, take note of how your interest rate is being calculated. Usually, this is a fixed rate the bank offers to you when you apply for your home loan, which can be as high as 18%. Ultimately, the less often you must pay for interest, the better. Keep an eye open for the above and make sure you find what works best for you.

Rule 3

Fixed vs. Adjustable Rate: Know the Difference

Before you take on a loan, be mindful that there are two types of interest rates. If you take on a fixed-rate mortgage, then your interest rate will not change throughout your loan repayment. As such, your monthly principal and interest payments will remain consistent throughout the tenure of your loan. An adjustable-rate mortgage, in contrast, can rise or fall in accordance with the prevailing market interest rates.

Rule 4

Fees, Fees, Fees

In addition to the base price of the property, you will also have to account for several extra fees.

These include:

The home loan application fees and legal fees

Banks will often require you to pay 1% of the total loan in order to cover the charges incurred for valuations and for processing the loan. Additionally, you will also need to pay around $250 per title deed for legal service.

Ownership transfer tax fee

When property ownership is transferred from the seller to the new owner, a tax fee is being applied. The tax fee must be paid to the respective city or province the property is located in. Thus, as the buyer, you will need to pay 4% of the ownership transfer fee, as well as $1,000 for the services of a cadastral office.

Home insurance fee

Cambodia's Ministry of Economy and Finance has made it compulsory for buyers to have a home insurance should they plan to take up a mortgage loan. The fee for that home insurance will depend on the size and value of your property. If you are planning to get a property that is valued at more than $100,000, you will have to pay a home insurance fee of $100 (or higher) annually. However, for properties priced below $100,000, the fee will be less than $100.

Real estate agent’s fee.

The real estate agent’s fee is usually shouldered by the seller of the property. However, in selected situations, it may be charged to the buyer instead. Such situations include cases where the seller is unwilling to sell, but the buyer contracts an agency to persuade the seller. The commission fee for real estate agents typically stands at 3% of the property price. However, the real estate agent fee is not always incurred, but may vary depending on your situation. For instance, if the buyer purchases a property directly from the property developer, this fee will not be incurred.

Rule 5

Knowledge is Your Friend

As different banks offer different rates, it’s good to do some research and make comparisons before applying for a loan. Don’t be afraid to reach out directly to a bank representative whenever you have questions. Another great tip is utilising a loan calculator spreadsheet online to tabulate different scenarios and compare the rates that you need to pay.

Rule 6

Read the Fine Print

You’ll notice that there will be fine print detailing terms and conditions in your loan documents. These terms and conditions usually consist of additional charges such as stamp duties, redemption letter fees and so on. Make sure you take the time to read through them thoroughly and understand everything written. Though it might take a while to get through everything, it’ll be worth it as you don’t want to run into surprises after signing up.

Rule 7

Don’t Hesitate to Negotiate

Lastly, do not hesitate to negotiate with the bank to reduce your loan interest or revise your loan package after a few years. If you have solid proof that another bank can offer you a better rate, ask your bank to consider reducing theirs. Alternatively, you may try to negotiate and change a different loan package within the same bank too! This will require you to have an existing relationship with your bank as it is easier for them to track your financial records. One important point, be sure to ask if this will incur any additional fees.

At the end of the day, taking a mortgage is all about planning. We advise everyone to always think about existing financial obligations while doing thorough research before deciding. Falling behind on your loan repayments may cause you to incur late payment penalties, or even worse, cause the bank to seize your home. It is important to borrow responsibly so that the dream of buying a house does not become a nightmare instead.