Financial terms can be daunting. It doesn’t help when there are hundreds more of them.

Good news is, you don’t necessarily need to know all of them, but learning some of the more common ones might just benefit you. You’re probably familiar with terms like credit score or interest by now, but today we’re going to add another financial term to your vocabulary and that is – the Debt-to-Income Ratio or commonly known as DTI.

Yes, it sounds intimidating but before you click the exit button, you should know that your DTI plays quite a fundamental role in your finances, especially if you’re looking to take a loan. Don’t worry, as usual, we’ll run you through the basics so that you can understand this term better. Let’s begin!

Understanding the Basics of DTI

Your debt-to-income (DTI) is a ratio that compares your monthly debt expenses to your monthly gross income. A more layman term to explain this would be that the DTI is the percentage of your income that goes to paying off your monthly debt payments like your student loan, mortgage debt, credit card bills, and so on. Okay, great so why do you need to know this?

Why is It DTI Important?

This financial formula is one of the best debt assistants you can ever hire without paying. The DTI formula is like Charles Xavier from X-men, believe it or not. It is able to tell you if you’re able to financially take on another loan so that you avoid the potential of getting into more debt than you can handle. In short, DTI is a good rule of thumb to guide your personal balance between debt and income. That’s because when you use the DTI equation, you can calculate your DTI before and after taking a new loan. For instance, if taking a new loan means forking out more than you should of your current income, this gives you an indication that you might want to wait on taking a new loan. Hence, the DTI gives you a good idea if taking a new loan is something you can bare financially. See how useful this is? This nifty tool gives you the power to save yourself from future financial constraints!

Additionally, since Cambodia is moving towards building a more solid banking system, such as implementing credit report checks, understanding where you’re at financially (using the DTI formula) can help you apply for a loan with a higher chance of getting it approved. You could even use this simple calculation as a financial measure that’ll assist them in determining if you’re qualified for a new loan!

But what does a “good” DTI ratio look like? How do you know that you’re in reasonable state to take on more debt? Don’t worry, we’ve got that covered later. Just keep reading!

How to Calculate Debt-To-Income Ratio?

Now that you have a better idea of what the debt-to-income ratio is, it’s time to calculate yours. For starters, you may start accumulating all your monthly recurring debts such as your student loan, credit card bills, mortgage debt, and other monthly obligations. You can list them on a paper to make sure that you’ve compiled all your debt expenses. This way you’re 100% sure that you did not miss out on anything.

Next, similarly to what you’ve done for debts, do it for your total monthly income before interest or tax deduction. This includes your employment salary, bonuses, passive income, side gig income, and other sources. You may place them side by side to your debt list. As long as everything is stated clearly.

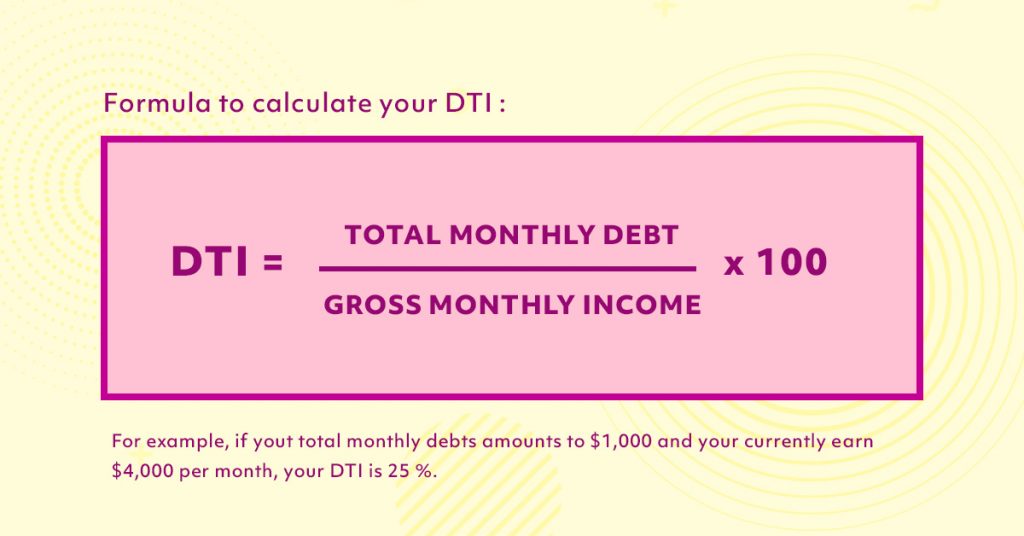

Once you’ve got a total sum of both your monthly debt and gross income, use the DTI formula! Here’s an example calculation

Debt to Income Ratio (DTI) = Total recurring monthly debt/ Gross monthly income x 100

Total monthly debt: $2,000

Gross monthly income: $5,000

DTI Percentage = 40% But wait, what does 40% possibly mean?

Understanding Your Debt to Income (DTI) Ratio

Once you know how to use the DTI formula, you’ll be able to tell if your income can support the next loan you’re taking. How do you know if your DTI percentage is good news or bad? We’ve broken this down into 4 category readings to help you better understand what your DTI percentage means.

Optimum – 36% or less

First things first, you would always want to have a percentage of no more than 36% because this is the optimal level of a DTI. This simply indicates that 36% of your income goes to paying off debt. This way you’ll still have enough to support your other financial needs like contributing to your savings account. If you fall under this range, try to avoid incurring an overly high amount of debt to maintain a good DTI ratio. Since this illustrates a good percentage of DTI, your loan application (if any) will have a higher chance of being approved as it assures the lender that you’re capable of repaying your loans on time.

Moderate – 37% to 42%

Although this is not an alarming state, it could be better. If you fall within this range, your DTI indicates that about one-third of your income is spent on repaying debts. In this situation, you may either choose to find ways to quicken your debt repayment or increase your income to reach the optimum level of DTI.

High – 43% or 49%

If your calculation falls within this range, you might want to start addressing your debt issue before it escalates further. If you find yourself in this situation, you’re encouraged to focus on paying off your current loans first before taking on a new loan. 43% – 49% DTI simply indicates that most of your income is currently dedicated to your debts. Remember, a DTI percentage that falls within this range may not only hurt your credit score, it may also threaten any loan opportunities you may decide to take in the near future.

Alarming – 50% or more

This is considered a financial critical situation. In the alarming stage, it means that more than half of your income goes toward debt payments each month. The best next thing you can do is to seek financial help. Trust us, there is no shame in this as you’re looking for ways to solve a problem. Hence, you’re doing the right thing! Keep in mind that if you let this situation escalate, you’re putting yourself at risk for bankruptcy which we believe, isn’t something that you want.

Always make sure to only apply for a loan that you can afford. There are many tools out there to manage your finances, especially in an era where there’s an app for everything! All you have to do is take 20-30 minutes a day and spend the time to learn how to better manage your personal finance. You’ll only have yourself to thank when you see great progress in building your wealth. If you’re interested to learn more about loans. we’ve made a video you can check out here.